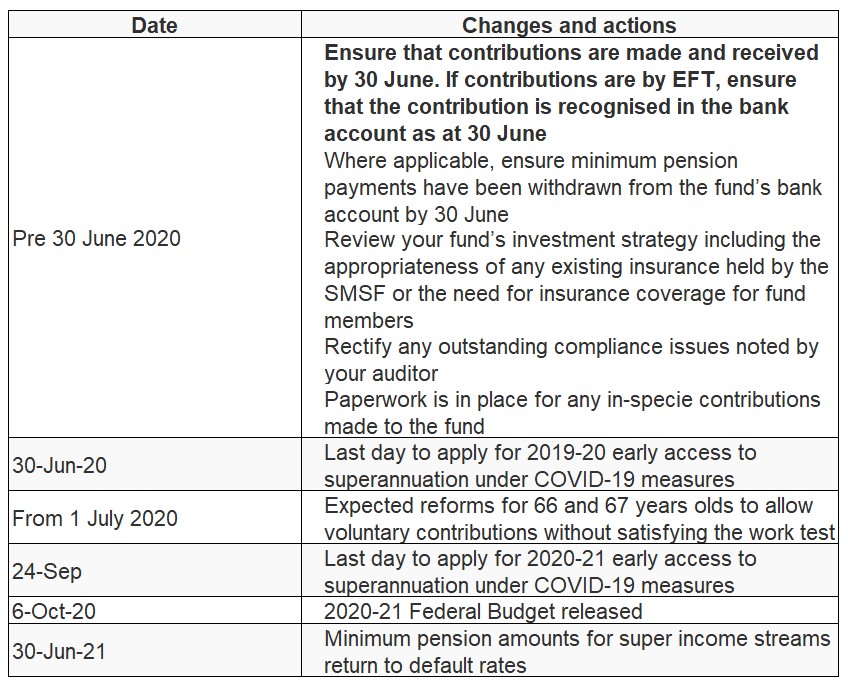

In brief

What’s new

2020-21 Federal Budget delayed until October

The release of the 2020-21 Federal Budget has been postponed from its traditional date in May until 6 October 2020. We expect there will be a number of reforms and measures to tighten spending, recover revenue, and range of productivity measures. We will keep you advised of significant changes that might impact on you and your company.

Early access to superannuation

Individuals in financial distress as a result of the coronavirus pandemic are able to self-certify and apply for early release of up to $10,000 of their superannuation in 2019-20, and again in 2020-21 (up until 24 September 2020).

To be eligible for early release, you should ensure you meet the eligibility criteria:

- You are unemployed, or

- You are eligible for jobseeker, parenting payment or special benefit or farm household allowance, or

- On or after 1 January 2020, you were made redundant, or

- Your working hours were reduced by 20% or more, or

- For sole traders, your income reduced by 20% or more.

The early release of superannuation measure is available to Australian citizens, permanent residents and New Zealand citizens with Australian held super. Eligible temporary visa holders can also apply for a single release of up to $10,000 before 1 July 2020.

We’ve had a number of questions from clients asking if they can access $10,000 of their superannuation in 2019-20 and 2020-21 and then recontribute the amount before the end of the financial year to claim a tax deduction.

If you have withdrawn more than you need, you can recontribute this amount under normal contribution rules. However, if you are withdrawing superannuation with the intent to recontribute the amounts to maximise your tax deductions, we advise against this as it will attract the ATO’s attention. If you have accessed your superannuation early and recontribute some or all of the amount, ensure that you have the documentation in place to prove that you met the eligibility criteria for early release and were in financial distress. Harsh penalties apply to those who make false declarations.

Funds cannot be released to members until the SMSF receives a release authority from the ATO enabling the withdrawal to be made.

In addition, you should ensure that there is documentation in place, such as a minute, noting the Commissioner’s determination and the release amount, confirmation of the members eligibility, and confirming that the governing rules of the fund allow for the release on compassionate grounds.

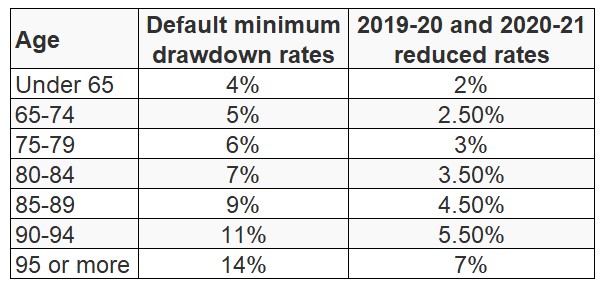

Minimum pension amounts for super income streams

The minimum drawdown requirements for account-based pensions and similar products have been reduced by 50% in 2019-20 and 2020-21. If you have already drawn down more than the required minimum, any deposits into your fund will be treated as a contribution under normal contribution rules.

SMSF compliance status removed if annual returns late

If your SMSFs annual return is more than two weeks overdue and you have not requested a deferral, the ATO will move your fund’s status on Super Fund Lookup from ‘Complying’ to 'Regulation details removed'.

Broadly, the change may result in the fund not receiving rollovers from APRA regulated funds and contributions from employers. Having a status of 'Regulation details removed' means APRA funds won't rollover any member benefits to the SMSF and employers won't make any super guarantee (SG) contribution payments for members of the SMSF.

This could particularly impact on those consolidating their superannuation accounts or receiving mandated employer contributions from independent employers (note that employees are required to advise their employer if the fund is no longer complying). There is also a risk that related employers could face issues as a result of making contributions to a fund that is not confirmed to be complying, such as losing the deductibility of contributions and incurring super guarantee charge obligations.

The due date for most 2018-19 returns is 5 June 2020 this year unless the fund has outstanding returns (then the due date is 15 May 2020).

Impending changes

Greater flexibility for those over 65

Reforms before Parliament will give greater flexibility to those aged 65 and over to make voluntary superannuation contributions.

For those under 67 years of age, the reforms will enable you to:

- Make voluntary superannuation contributions (concessional and non-concessional) without meeting the Work Test. Currently, voluntary contributions can only be made if the individual has worked a minimum of 40 hours over a 30 day period (Work Test).

- Use the ‘bring forward rule’ to make up to three years of non-concessional contributions. That is, you can make non-concessional contributions of up to $300,000 from the 2020-21 financial year.

In addition, the cut off age for making voluntary contributions for your spouse will increase from 70 to 75 years of age.

These reforms are not yet law and you should not act on them. We will keep you up to date on the status of this legislation.

Fund housekeeping

Warning on non-arms length income expenditure

From 1 July 2018, the definition of non-arm’s length income (NALI) expanded to manage a loophole that allowed superannuation savings to be artificially inflated by non-arms length expenses that were provided free or at below market rates. For example, where services were provided to the fund by a company related to a fund member at reduced rates. In this way, funds could increase their superannuation savings while circumventing the contribution caps.

Where this situation arises, the rules tax this non-arms length income at the top marginal tax rate.

The question of whether the non-arm’s length income rules apply depends on the capacity in which the trustee undertakes those activities. Essentially, if you or a related entity are providing services to your superannuation fund in a capacity other than as trustee, and you (or the related entity) currently provide that service to the public, an arms length fee should be charged for this service. Failure to do so could result in non-arms length income applying to the applicable asset the expense relates to.

There has been a lot of confusion over the new rules and the ATO has stated that they will not commit compliance resources to this issue until 1 July 2020. This gives trustees a limited opportunity to ensure that any non-arms length services provided are at market rates. If you are uncertain, please contact us and we can work with you to ensure your fund is not at risk.

Carry forward unused concessional contributions

If you have unused concessional contributions, that is, you did not contribute the full $25,000 in 2018-19 or 2019-20, then you can carry forward these amounts for five years on a rolling basis if your total superannuation balance is below $500,000 on 30 June (of the year you intend to access the unused amount).

The ability to carry forward concessional contributions applies from 1 July 2018, with 2019-20 financial year being the first year an individual can access their unused carry forward concessional amount.

Concessional contributions include employer contributions (super guarantee and salary sacrifice) and personal contributions where you have claimed a tax deduction.

For example, if your total concessional contributions in the 2019-20 financial year were $10,000 and you meet the eligibility criteria, then you can carry forward the unused $15,000. You may then be able to make a higher deductible personal contribution in a later financial year. If you are selling an asset and likely to make a taxable capital gain, a higher deductible personal contribution may assist in reducing your tax liability in the year of sale.

Remember:

- Your total superannuation balance must be below $500,000 on 30 June of the prior year before you utilise any carried forward amount (within the 5 year term); and

- In some cases, an additional 15% tax can apply (30% total) to concessional contributions made to super where income and concessional contributions exceeds certain thresholds ($250,000 in 2019-20). Your income could be higher than usual in the year when you sell an asset for a capital gain.

This is an excellent concession to help you top up your superannuation.

Valuing SMSF assets

SMSFs are required to value their assets at market value. Depending on the situation, a market valuation may be undertaken by a:

- Registered valuer

- Professional valuation service provider

- Member of a recognised professional valuation body, or

- A person without formal valuation qualifications but who has specific experience or knowledge in a particular area.

For real property, the valuation may be undertaken by anyone as long it is based on objective and supportable data. A valuation undertaken by a property valuation service provider, including online services or a real estate agent is acceptable.

However, where the value of the asset represents a significant proportion of the fund’s value or where the nature of the asset indicates that the valuation is likely to be complex, you should consider the use of a qualified independent valuer.

In general, real estate does not necessarily need a formal valuation each year by a licenced valuer unless there is a significant event that occurs during the year which may affect the previous valuation. A significant event could be one that directly involves the property itself, the fund on a general level such as one of the fund’s members going into pension mode, or if the asset represents a significant portion of the fund’s value.

Contributions must be received by 30 June

To claim a tax deduction for super contributions (as an employer or as an individual), the payment needs to be received by the fund no later than 30 June. Merely incurring a liability is not enough.

If you are making a personal superannuation contribution that you want to claim as a tax deduction, you need to write to your fund in their approved form and advise them of the amount you intend to claim as a deduction. The superannuation fund then needs to acknowledge your notice of intent and agree to the amount you intend to claim as a deduction. This will normally be in the form of a notice or certificate from the fund to confirm the tax deductibility of the contribution.

Review and rectify any outstanding compliance issues

If your auditor has highlighted any breaches or issues in previous year fund audits, you should review and rectify these issues by 30 June. The penalty for illegal access to the SMSF’s funds without meeting a condition of release is $12,600 per trustee.

The ATO have a number of powers to address non-compliance:

- Education directions - require the trustee/director to complete an ATO approved education course within a specific timeframe. An administrative penalty of $2,100 applies for non-compliance.

- Rectification directions - requiring the SMSF’s trustee/director to take specific action to rectify the contravention within a specific timeframe.

- Administrative penalties - penalties from $1,050 to $12,600 apply to specific breaches. Each individual trustee is liable for the penalty and directors of a corporate trustee are jointly and severally liable. The penalties are payable by the trustee/ director and not refunded by the SMSF.

- Informal arrangements to rectify minor breaches.

- Enforceable undertakings.

- Disqualification of a trustee.

- Allowing the SMSF to wind up.

- Notice of non-compliance.

- Freezing an SMSF’s assets.

- Civil and criminal penalties where the fund:

- Breaches the sole purpose test.

- Lends to members of the fund.

- Breaches the borrowing rules.

- Breaches the in-house asset rules.

- Enters into prohibited avoidance schemes.

- Fails to notify the regulator of significant adverse events.

- Breaches the arm's length rules for an investment.

- Promotes an illegal early release scheme.

These powers also enable the ATO to look back to any breaches from previous years that were unresolved at 30 June 2020.

Review the fund’s investment strategy

Trustees are required to ‘regularly review’ the fund’s investment strategy. We recommend that trustees review the strategy and document the review at least annually or when the circumstances of the fund change.

Where an SMSF has entered into a borrowing arrangement to acquire an asset, trustees should seek advice to structure insurance cover either inside or outside the SMSF to assist in meeting the on-going obligations of the debt repayments. The fund’s ability to meet the on-going debt repayments can be severely jeopardised where one member of the fund dies, as the fund may have needed to utilise contributions that were being made for that member to meet the repayments. Such a scenario could result in the fund having to sell the property.

Review insurance inside your SMSF

SMSF trustees need to consider the need for insurance cover for the fund members when formulating and reviewing the fund’s investment strategy.

Superannuation funds are only able to offer or take out new insurance cover where the definitions are consistent with the death, terminal illness, permanent incapacity and temporary incapacity conditions of release under the Superannuation Industry Supervision Act.

It’s important that you review insurance inside your SMSF not just for compliance with the law but also effectiveness. An important issue to consider is how any insurance inside your fund should be structured; that is, from where the premiums are paid from the fund and what account any policy proceeds will be paid to inside the fund.

Correctly structuring insurance inside your fund can be complex. We recommend that SMSF Trustees seek the advice of their financial adviser to achieve the most tax effective outcomes for insurance proceeds, especially on the death of a member.

Lodgement deferrals

The ATO has automatically deferred 2018-19 SMSF annual returns lodged through a tax agent from 15 May and 5 June until 30 June 2020 unless the fund has outstanding returns (then the due date is 15 May 2020).

Contributions you didn’t know you made

A contribution to a fund can be more than just a deposit of money into the bank account of a superannuation fund. It could include:

- Money

- In-specie asset transfers

- Paying fund expenses

- Increasing the value of a fund asset

- Forgiving a fund’s debt

- Meeting a fund liability

- Rendering services to the fund at less than market value

- Guarantor arrangements

- Some Discretionary Trust distributions

Trustees can often be surprised by what is considered to be a contribution, for example:

- In-specie transfer - If an asset is transferred or acquired from a related party for less than fair market value, the difference may be treated as a contribution.

- Capital improvements - Capital improvements to existing fund assets for no consideration or less than arm’s length consideration may be treated as a contribution.

- Debt forgiveness - A contribution is made if a loan, entered into by the fund is forgiven by the lender (related party). The contribution is made when the deed of release is executed that then relieves the fund from the obligation of repaying the debt.

- Guarantor arrangements - A contribution occurs if a guarantor to a debt of the fund (trustees in their own right) satisfies a loan obligation of the fund and then forgoes the right of redemption against the fund (trustees) itself.