Tax deductions denied

If taxpayers do not meet their PAYG withholding tax obligations, from 1 July 2019 they will not be able to claim a tax deduction for payments:

· of salary, wages, commissions, bonuses or allowances to an employee;

· of directors’ fees;

· to a religious practitioner;

· under a labour hire arrangement; or

· made for services where the supplier does not provide their ABN.

The main exception is where you realised there is a mistake and voluntarily corrected it. For example, if you made payments to a contractor but then later realised that they should have been paid as an employee and no PAYG was withheld. In these circumstances, a deduction may still be available if you voluntarily correct the problem but penalties may still apply for the failure to withhold the correct amount of tax.

Are you in the road freight, IT or security, investigation or surveillance business?

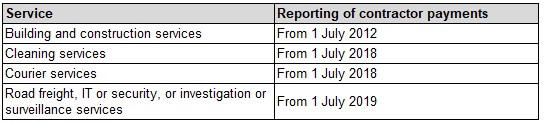

The Taxable Payments Reporting system was introduced to stem the flow of cash payments to contractors and rampant under reporting of income. Since the building and construction industry was first targeted in 2012, the reporting system has expanded to include cleaning and courier services. Now, a broader set of industries have been targeted.

If you have an ABN, and are in road freight, IT or security, investigation or surveillance, then any payments you make to contractors will need to be reported to the Australian Tax Office (ATO).

Be careful here as the definition of these industries is very broad. For example, ‘investigation or surveillance’ includes locksmiths. The definition covers services that provide “protection from, or measures taken against, injury, damage, espionage, theft, infiltration, sabotage or the like.”

IT services are the provision of “expertise in relation to computer hardware or software to meet the needs of a client.” This includes software installation, web design, computer facilities management, software simulation and testing. It does not include the sale of software or lease of hardware.

Road freight is typically goods transported in bulk using large vehicles. This includes services such as log haulage, road freight forwarding, taxi trucks, furniture removal, and road vehicle towing. The addition of road freight to the taxable payments reporting system completes the coverage of delivery and logistics services as businesses in courier services are already obliged to report payments to contractors to the ATO.

If your business is impacted by these changes, you need to document the ABN, name and address, and gross amount paid to contractors from 1 July 2019. Your first report to the ATO, the Taxable Payments Annual Report (TPAR), is due by 28 August 2020. This might seem like a long way away but it will come around quickly and you need to ensure that your systems are in place to manage the reporting required easily and accurately.

Who needs to report?

The obligation to report contractor payments to the ATO is already quite broad. The addition of road freight, IT or security, or investigation or surveillance services, adds another layer.

For businesses providing mixed services, if 10% or more of your GST turnover is made up of affected services, then you will need to report the contractor payments to the ATO.